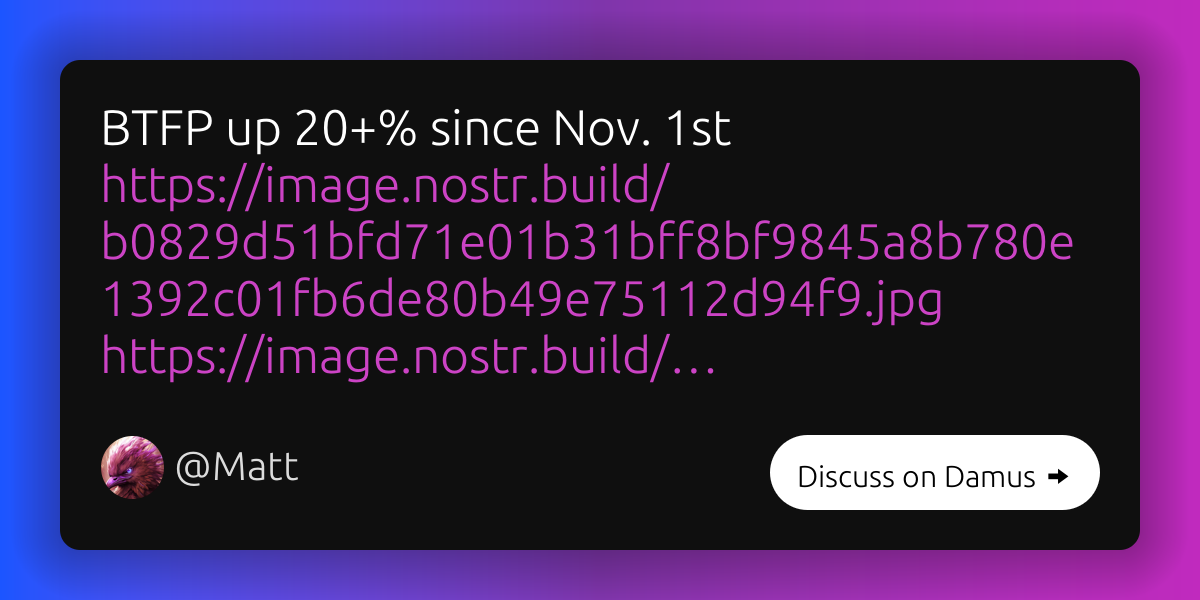

The Fed's Bank Term Funding Program (BTFP), the facility that they introduced after the March 2023 banking crisis, now offers lower borrowing rates than the Fed pays in interest on reserve balances.

So, banks are arbitraging this by borrowing from the facility (i.e. from the Fed) at one interest rate, and then depositing that borrowed money with the Fed to earn a higher interest rate, and thus are earning that risk-free spread. They're arbitraging the Fed.