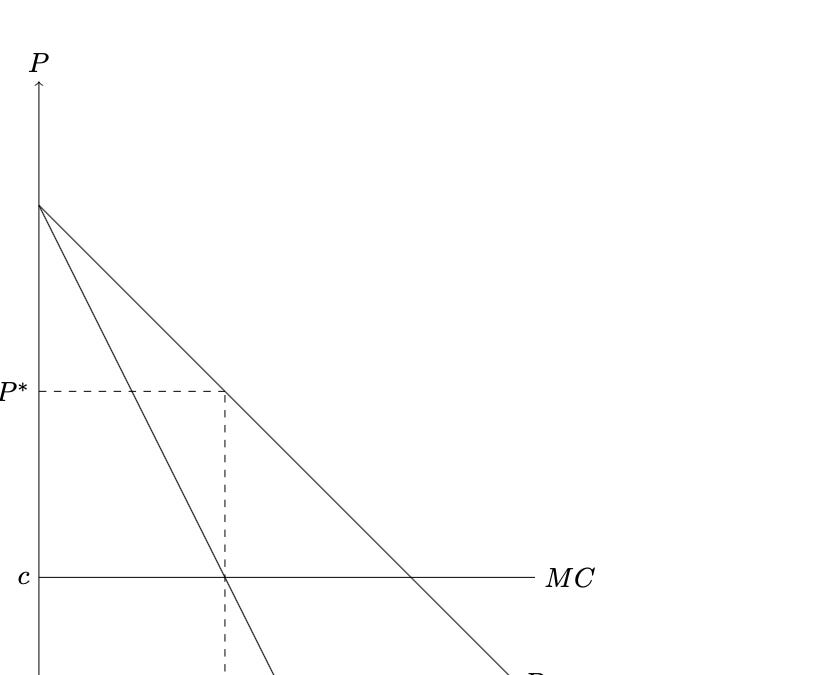

People are desperate to blame inflation on anything but Federal Reserve policy. They’d rather blame greedy corporations. Some people even point to rising markups of prices over costs as evidence that this is all just greed. But some basic knowledge of price theory tells us that if markups are rising, this is driven by demand and, in particular, expansionary monetary policy.

The trillion dollar coin idea to “solve” the debt ceiling would basically just have the Fed operate like FTX — worthless tokens as assets, immune from market valuations. Also, like FTX, this trick would make the central bank insolvent.

Central bankers continue to use the Phillips Curve as a guide for monetary policy. This demonstrates a basic lack of understanding about the Phillips Curve itself and the last 50 years of macroeconomic theory.

The conventional wisdom on historical asset bubbles is that these were episodes of irrational exuberance. In reality, historical asset bubbles were much more interesting. The South Sea Bubble and the Mississippi Bubble were the end result of government debt consolidation schemes.

Tulipmania was an artifact. There was no bubble. The Dutch elite passed legislation that turned futures contracts into options contracts.

Economists routinely talk about the problems associated with monopoly, but there’s one monopoly that goes unquestioned: the monopoly on currency issuance.

The Fed is like a child trying to build the tallest tower of blocks. Each new lending facility adds a block to the tower. Each new block makes the tower look more impressive. But the taller the tower, the less stable the tower becomes and the more likely a small shock can bring the whole tower crashing down.

It’s become increasingly evident to people that we're on an unsustainable path.

The Fed continues to expand the scope of its operations. A new problem? Here's a new facility to deal with that. This makes the operations more and more complex, which makes the institution and the financial system more fragile.

The Fed's balance sheet is going to continue to get bigger and that will lead to more politicization. And the balance sheet is going to get riskier as these facilities simply transfer the risk from the financial system to the Fed.

I’ve been around long enough to have read Burniske’s book on “Cryptoassets.” The book had a valuation model for these assets that was essentially nonsensical. Of course, he wrote it so early that prices of each of these assets is much higher than they were then. This gives him validation, but it’s false validation. Like the guy who successfully predicted the stock market crash of 1929 by applying the law of gravity to stock prices, this won’t end well for him.